As we wind down 2015, I wanted to take a look back at the Goals for the year and how we did. I’m also going to talk about what went well, what didn’t, and a few of the surprises along the way.

This may be the first year of my life that I’ve ever been able to view my financial health holistically. It’s also the first time that I’ve ever written down financial goals for myself. I’ve tracked every dollar each month as well as goal progress along the way. Sitting down and Drawing My Picture has been a powerful tool indeed.

Financial Goals 2015

I started the year with three pretty basic and achievable goals.

- Reduce overall outstanding debt (including mortgage) by 10%.

- Make contributions to investments (taxable and retirement) of 10% of salary.

- Eliminate any monthly interest payments due to credit cards.

In 2014, I had only managed to reduce my overall debt by a little more than 2%. Not wanting to spend another 49 years working on the problem I set my sights on 10%

I also wanted to continue to contribute to investments at least a little. I had a general idea of how much I would be making over the course of the year and what my previous year’s total spending was so I also set a 10% goal (pre-tax included) here. I did reduce my 401k contribution and increase my ESPP contribution to help generate some extra income for debt reduction.

Coming into 2015, I had pre-existing credit card balances of approximately $20,800. Towards the end of 2014, I had done some balance transfers to 0% offers so $12,300 of that total was not generating interest and $8500 was. Tackling the $8500 was my top priority since it was costing me an extra $180 per month in interest.

I’m happy to report that at the time of writing, all goals have been met for the year. Debt reduction is at 10.65%, investment contributions are at 10.38%, and I only paid interest on a credit card four months out of the year. I thought I had eliminated interest after March, but the extra Vet bill led to a $38 charge on the November statement.

Year-End Balance Sheet

Let’s take a look at the balance sheet for the year. I’ve intentionally left out the cash accounts (Checking/Saving) since these have relatively low balances and will fluctuate a bit by year end.

The ‘Other Assets’ listed is the estimated value of our house according to Zillow. I hesitate to use it in the balance sheet since it is an estimate and not a very liquid asset at all. Asset value increased by 7.53% this year which is mostly due to contributions and an increase in estimated home value.

The remaining $7180 of credit card debt is sitting on a balance transfer card with a 0% introductory rate that will expire sometime in January. I need to review the terms of the transfer and make a plan to deal with that before the interest starts. I do have an ESPP coming up on Jan 31 that will eliminate the balance if everything goes according to plan.

Overall Net Worth increased by 44.32%. That’s a really incredible number to see, but it makes sense when you look at the fact that I’m both adding assets and decreasing liabilities.

Cash Flow

This is the first year that I’ve tracked Cash Flow. I can say that I was very surprised to see the numbers at the end of the year. It’s eye-opening (and slightly alarming) how much money is going out the door. Here’s a summary (Income and Investments include pre-tax contributions to retirement accounts)

I’m confident that we can lower expenses next year. Right away, I know that we’ll be spending around $6000 less on outstanding credit card debt (~$13000 this year with $7180 remaining). We also had two larger purchases of a replacement laptop ($3000) and a Vet bill ($4000).

It’s possible that I can be a little more aggressive with my goals for 2016, but I don’t want to set myself up for failure so I’m still working on finding a balance. We may also be able to fund a family vacation next year which will help with the mental health aspect for the rest of the family (I think I’ve only taken 5 or 6 days off this year).

The slightly alarming bit is the fact that our total income included bonuses and RSU sales. If it hadn’t been for that, we may have ended up adding to debt instead of removing it. I need to get us to a point where we’re not dependent on extra income and everything can be handled by regular salary.

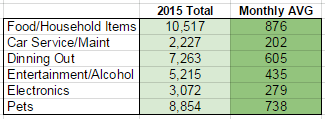

Expenses We Can Control

There are a few areas of expense where I know we can make a difference. I tallied up the monthly average for variable expenses and found the following items are over budget on average:

Pets and Electronics both have outliers that are skewing the average. Both should be much lower next year. The top item is basically anything we buy at the grocery store. We’re only slightly over budget on that but if we can cut it by 10% that’s around $1000 in savings.

Dining out should be half of what it is. One of the key challenges for us is having a weekly menu and getting the grocery run done. If we can make a better effort to be consistent there then we can easily cut this in half and save $3500 or so.

Entertainment and Alcohol includes things like movies and hockey tickets as well as trips to the package store. I’m cutting back on the craft beer and will be re-focusing some hobby time to brewing again in 2016. Honestly, I’d like to see this number cut in half too but a 10-20% reduction will be great.

Combine those reductions with the unexpected expenses and credit card payoff and we could reduce expense by up $18000. Stretch goal would be to make it under $100000 total expenses for the year, but we are still in debt reduction mode so I’m not as focused on that.

2015 – Year of Success

Well there you have it. As of right now, it looks like I was able to meet my financial goals for the year. Woohoo!

I’m looking forward to 2016 and will be updating my goals for the new year in a few days.

Cheers!

-cb3