Deciding What’s Next (Financially)

Over the past couple of month’s I’ve been mulling over a couple of ideas in regards to the next steps of my financial plan and pursuit of Financial Independence (and possibly Retire Early). Now that we’re down to a single debt with our mortgage, I need to re-analyze our current state and adjust some of the sliders. Our Next Life had an excellent post about how their goals changed over the course of implementing their plan. For me, debt removal was a goal, but not necessarily the goal post.

Hopefully over the course of this post, I can take a look at the current goals as well as the new goals that I’m considering and discuss what I need to adjust to accomplish them.

Here’s where we were…

Debt payoff

When I started really tracking my debt situation at then end of 2014, we had accumulated around $230,000 in total liabilities. That was a combination of mortgage, student loans, personal loans, and credit card debt. Once upon a time, I thought this was pretty reasonable although my perspective may have been skewed due to working with so many folks in the SF Bay area.

Luckily I came to my senses and realized I needed to do something about it. My original plan was to shoot for 10% of the total per year. 2015 was a success and we eliminated a little over that with a 10.65% reduction. This year, I needed to target 15% of the remaining balance to stay on track. I’ve closed every balance but the mortgage an we’re on target for a 17.73% drop this year! That’s a little over $60k worth of debt gone in two short years.

Taking those items off of the balance sheet gives me around $30k of free cash flow next year (assuming no major life changes) that I need to reallocate. I just need to figure out where to send it.

Here are the things I’m considering…

Home Repairs

This one is inevitable when you own a home. Eventually, something is going to require a larger sum of money to repair. It’s really annoying, because it came up just after making all of this super progress. Chalk one up to Murphy.

The good news is that I can handle the cost of the project. I’ve got to get some siding repaired (ours is cedar), exterior paint done, and some deck repairs done. There’s also some cabinetry repair in the kitchen as well as some drywall repair and interior paint touch-up.

The bad news is that the work on the exterior really needs to be done now, but the cash won’t be available until Feb of next year. I’m going to solve this with a Home Equity Line of Credit with the knowledge that I will be able to re-pay that in a few months. This will keep the interest payments to a minimum.

That eats up between $10-15k. Annoying but necessary.

Investment Contributions

In order to make a decision about investment contributions, I need to understand where I am and what my goals are. Ideally, I’d like to be FI by the time I’m 50. That gives me eight years to build (I turn 42 this week). That’s the goal, but where do I stand?

If I look at the statistics for the average American, I see that folks in my age group have a mean savings of around $63000. Woohoo! I have a little over $170k depending on where the market happens to land today. That’s almost three times as much as my peers, but it doesn’t give me the warm fuzzies since I don’t want to wait until 65 to retire.

I need to do a really thorough analysis of what a FIRE life would look like for me. I’ve seen several examples on other blogs and need to take the time for it. For now, I’m just going to plug in to one of the simple retirement calculators that one can find through Google.

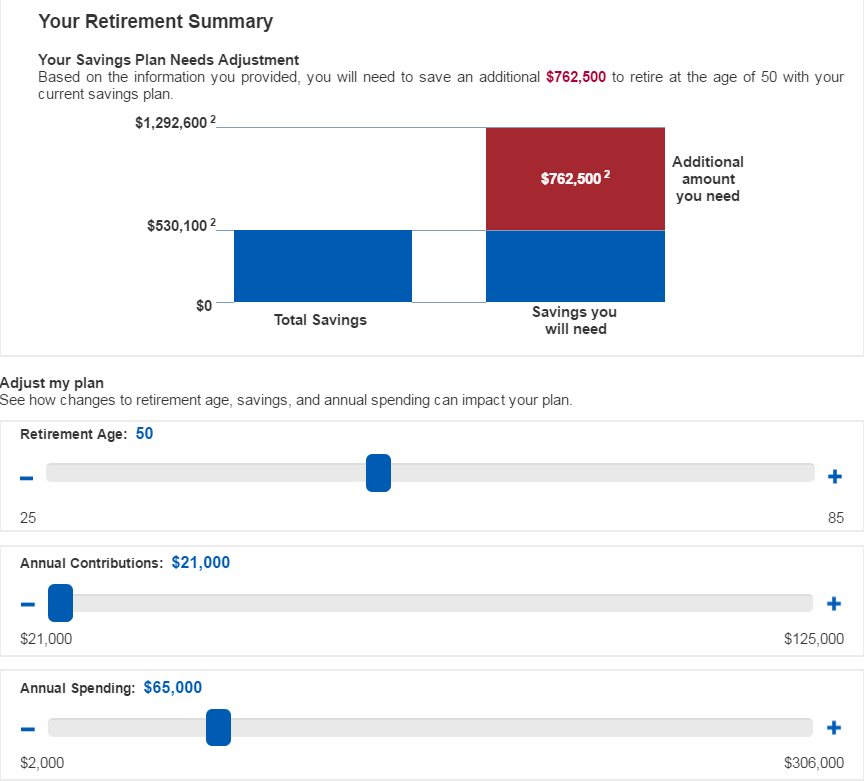

It was hard to find one that actually let me put in the exact numbers I needed as in how much income I need post retirement (60% of my salary is still too much). Schwab has a tool that let’s me do just that so that’s where I started.

My current spending per year (that isn’t debt payment) is around 55% of my gross income. That’s around $85,000 for a family of 4. I’m planning to reduce that to $65,000 per year which is much more reasonable (this will also free up more cash flow as we move in that direction). With my current yearly contributions of $21k and planned retirement age of 50, I’m told I have a shortfall of $762,500.  Shit! That’s a lot of money to conjure in the next 8 years. Obviously some adjustments are in order. If I adjust the contributions up to $44k and add an additional four years to make my retirement at 54, then I can get it to the point where I have a surplus.

Shit! That’s a lot of money to conjure in the next 8 years. Obviously some adjustments are in order. If I adjust the contributions up to $44k and add an additional four years to make my retirement at 54, then I can get it to the point where I have a surplus.

Now, this isn’t exactly ideal and the tool does make some assumptions about life expectancy, investment gains, and inflation but as a basic starting point it gets the point across.

New goal: Save at least $44,000 (that’s $23k of my cash surplus next year) per year going forward!

Diving Into Rental Property

I’ve also been thinking a lot about my asset allocation and how it’s almost all in the stock/bond market right now (If I don’t count my home as an asset). I’ve been including the house in the Net Worth calculation, but don’t really consider it an asset since it doesn’t generate income and I would still take a loss if I sold now considering loan + interest.

It’s not high priority by any stretch, but I know that I could put together the funds to purchase a smaller rental and get started in that market. I’m currently in research mode on this topic and trying to learn as much as possible before pulling the trigger.

Stay tuned.

Additional Mortgage Payments

This is apparently a hotly debated topic. Many argue that if interest rates on the loan are low and the market is favorable then money is better allocated towards investments. Money spent towards extra mortgage payments also ties up capital in an illiquid asset. Depending on one’s financial health, liquidity may or may not be a concern.

The other side of the coin that I see is the amount of money that I’m spending on interest. With a somewhat reasonable rate on a 30 year fixed loan of 5.25%, I would end up spending an additional 96% of my original loan value on interest! That basically doubles what I’ve paid for the house. Insane!

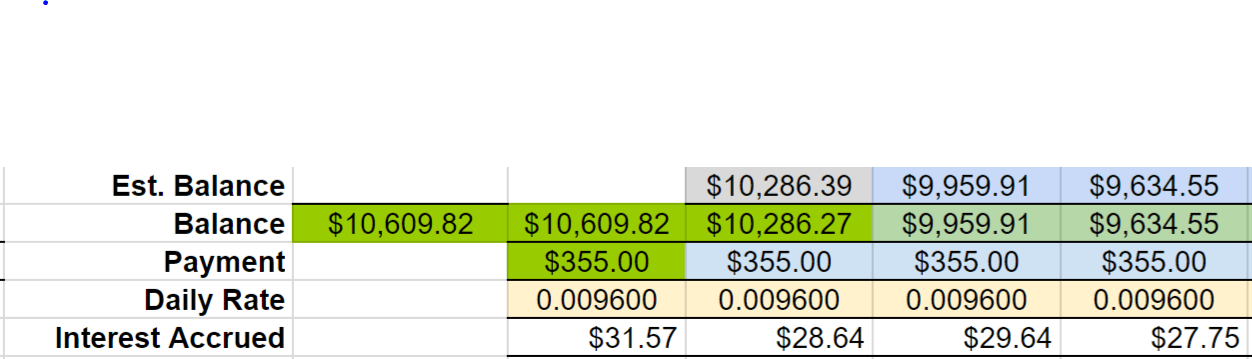

So far, I’ve managed to get a little bit ahead on the loan. Over the entire duration, I’ve been spending a little over $6 towards the principal. Since I paid the car and personal loan off this fall, I’ve used some of the extra cash flow and made almost a full payment extra toward principal (~$1250).

Now, the neat thing about this is when I look at an amortization table for my loan. With just this little bit extra, I have cut ten months from the loan as well as around $2000 worth of total interest. That’s OK, but not great.

Now, if I can maintain the extra $500/month towards principal then things get really interesting. My projected payoff date would move from Oct. 2039 to Dec. 2028 shaving eleven years off the life of the loan! That also reduces the total interest paid to 66% of the original loan amount. That would only take $6000 of my free cash flow to accomlish. Sweet!

College Savings

The last topic is also somewhat of a debate (not as hotly debated though). We both agree that we want to provide for our children’s education. The debatable part is how much and to what limit.

We both come from slightly different educational paths but are both college graduates. My degree took me through four different schools and I sampled both public and private as well as four year university and two year community college. Her path consisted of two degrees; one from a private university and one from a public university.

My current leaning is to do my best to fund an education from an in-state public school. Ideally, they can get some credits at a two year school and then move to the bigger school to complete their degree focus. I have 9-10 years for the first and 13-14 for the second to work on it and I’m estimating around $15k/year which would take $60k for each child under ideal conditions. I know this is probably going to go up, but I have to start somewhere.

Not counting for investment gains and assuming I’m starting from scratch, I need to put away $6000 per year for the first child and $4600 for the second. We will also be asking grandparents to contribute to this goal going forward.

Which Way to Head

Well, what would you do? I’ve obviously come up with more options that the $30k worth of cash flow that I’m freeing up next year. I’m also assuming that nothing major happens anytime soon to cause a large unexpected expense. It’s a lot to think about.

Cheers!

-cb3

Put a little bit towards each or focus on one area more than others? Let me know your thoughts.