Where’d We Leave Off?

Last time we talked, I was sitting at the beach about to take the kids swimming. It’s hard to believe it’s been over three months since I sat down to write.

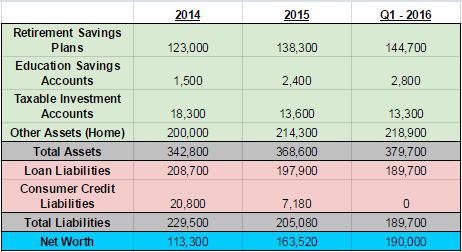

The financial progress was going well and we used our extra income to pay off another loan and go on vacation. The vacation went really well and was mostly relaxing. I only got one work call the whole week that we were away and it turned out to be very easy to solve over the phone.

We set our sights on finishing out the school year and looked forward to a hiking trip on the Appalachian Trail in June. This would be our first full vacation without children in almost 10 years.

Why the Time Away?

There have been several reasons for the extended absence. I could blame it on work getting busy (which it did), end of school year activities (which we had), or a host of other inconveniences that have occurred. The reality is, however, that my heart just hasn’t been in it.

I’m sitting with a lack of motivation at the moment that’s due in part to some imbalanced in my marriage. I’m torn with how much to share on the topic, but my wife and I have some extra challenges that make things difficult at times.

Having a set of goals and working really hard towards them and then realizing that your partner isn’t on the same page can really suck the wind out of the sails.

So, I took a step back to focus on that.

Some of the Challenge

You see, as with any relationship, there are areas where we see eye to eye and then there are some areas where we have completely different outlooks and world views.

She is very much a live for today type of person. I worry about and plan for the future. What’s interesting is how it reverses when it comes to going on adventures. She plans the trip details and packing list and checks everything off. I tend to throw things together-ish and rush out the door. We complement each other well in these areas.

We’re raising two children together. It takes a lot of time and energy and can be quite frustrating but overall, I think we’re doing an OK job. We also complement each other in our family management skills. She teaches independence and respect for one’s environment (including tidying up skills) while I’m the more patient nurturer.

Other areas of our marriage have been non-existent for a couple of years now (for some very good reasons). In this, there is frustration for both of us. Life has become very business-like at times and I feel that it’s starting to take a toll.

Now, normally I just dive into the next task that needs doing and wouldn’t bother her with any of it. She sees right through me. She says it’s the way I carry myself, the way I don’t smile often. This is not the way I want to be. It’s not the way I used to be.

We’ve been asking a lot of questions of ourselves and each other lately. What do you want in life? What makes you happy? Why aren’t you doing those things now?

So, What’s Happening Now?

Obviously, there’s a lot that needs work. I need to focus on being more open about how I’m feeling by being honest with myself as well as my partner. I know that I am not comfortable at this point in my life and change is necessary.

The blog will continue to be an outlet but I may shift focus to more writing about the things I’m doing to bring happiness back into my life. There will still be some finance updates along the way, but maybe more quarterly than monthly. My next post will be an exercise in discovery of the things I find fulfilling and that are a source of joy for me. I also promised to post about the AT trip, so I look forward to that.

Please pardon if I’ve over shared. I”m not here to be a complainer. This is simply my life at the moment and I want to be transparent. It’s better for all of us.

Change begins Within

Peace

-cb3