In with a Bang

To say that I wasn’t ready for the holiday to end and work to being again would be putting it mildly. I could feel my body getting tense the day before. Now we’re back to the races and I get a little busier each week.

Of course, with the transition from holiday back to routine we let a lot of things slide. Grocery planning only got done one week out of the month. We also tried to cram in social nights with neighbors and friends to try to hold on to a little bit of the break feeling.

We also settled on a vacation for the year and will be heading to the beach during the kids’ spring break. The condo has been booked and we’re really looking forward to the trip.

Current Goal Status:

Financial goals:

- Reduce overall outstanding debt (including mortgage) by 15%.

- Debt reduction for the month was 0.54% which puts us on track for a 5.84% overall reduction for the year. This is currently below target, but we’re just getting started!

- Make contributions to investments (taxable and retirement) of 15% of salary.

- We contributed 11.90% of our January income to investment accounts including 401k, 529, ESPP, and Brokerage. This will increase next month since I increased my ESPP contribution and will also increase 401k in March.

- Eliminate outstanding credit card debt.

- I was happy to note that we did not get charged interest on the January statement for the balance transfer card even though the introductory period ended on Jan. 22.

- This balance should be paid off in Feb. by a combination of ESPP proceeds and other deferred compensation that comes on the 15th.

- Eliminate remaining student loan debt.

- The only progress this month was the regular payment leaving a balance of $5700.

- Make a contribution to an IRA.

- No progress here… yet!

- Generate revenue from a new income stream.

- No progress here… yet!

Expense Goals

Ok, so January flat out sucked for meeting these goals. Here’s the damage:

- Meet the $800 per month grocery budget

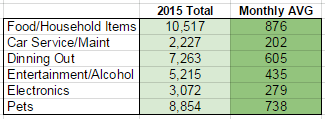

- We were over budget by $334. this is partially due to holiday spending and partially due to only planning weekly meals one week out of the month. Gotta do better.

- Reduce dining out to $400 per month (2015 – $600)

- We didn’t meet this one either, but we were under the 2015 average by $12. Woo! Again, a consequence of poor meal planning.

- Reduce entertainment/alcohol to $250 per month (2015 – $435)

- This one is also over budget by $265. Hosting social night gets expensive.

Personal Goals:

- Meditate at least three days a week

- I managed three days for the month. Work ramped up and I’m still not back on track for a good schedule.

- Take walks at least three days a week

- This I’ve managed to do and my step count is up to 60k per week. My average week in late 2015 was 45k steps.

- I’m also getting a ton of stairs going up and down the ladder for the DIY project.

- Spend at least seven days camping

- Nothing this month, but plans in place for June and maybe October.

- Go kayaking at least one time

- Brrr. Not yet

- Take one family vacation

- We booked a condo in St. Augustine where my wife used to go as a child. We also got a room for her parents to go along. This added $2200 to our expenses this month, but I know that cash is coming in to cover it.

DIY Project Update

Just a quick update on the progress for the living room renovation. In the two weeks that we’ve been working on the ceiling, I’ve managed to make it within a few rows of having one side done! That includes one false start where I made it about 16 rows up and we realized there was a mistake that made one end not align correctly.

I’m really happy with the way this is coming together. It looks much better than the stomp textured ceiling. We’re also going to be replacing the overhead lights and the ceiling fan. I’m estimating around $300-400 for the new fixtures.

I love power tools!

Get It Together

Ok, now that we’ve gotten over the holidays and have started getting back into the grind, I’m confident that we can do much better in February. The only thing that my put a little dent in our plan is that I’ve been asked to commute into the office two days a week. That’s an 18 mile drive which could mean thirty minutes or an hour and a half of driving each way.

Cheers!

-cb3