Bring on the New Year

Here we are. Already at the end of 2015. It’s hard to believe how fast this year has flown by. It’s also pretty cool that I’ve managed to track my expenses, stick to my plan and meet my goals for the year.

Now it’s time to formulate a new plan. I’m fairly confident that we could take the same goals from 2015 and re-apply them. After all, if I continue to do that then I’m only 9 years away from being debt free (In order to do that, I would need to reduce debt by 10% of the 2015 starting balance each year which is approximately $24k. If I use this years starting balance, I need 11.7% reduction to maintain the pace).

Accelerate the Finances

I’ve done a little back of the napkin analysis and based on a few factors, I think we can be more aggressive in 2016.

Financial goals:

- Reduce overall outstanding debt (including mortgage) by 15%.

- Make contributions to investments (taxable and retirement) of 15% of salary.

- Eliminate outstanding credit card debt.

- Eliminate remaining student loan debt.

- Make a contribution to an IRA.

- Generate revenue from a new income stream.

The first two are pretty simple and I believe easily accomplished based on what I learned last year. I’m trying not to spend extra income before it arrives, but I know what my ESPP and RSU schedule is and around how much I will receive. Most of that money is earmarked for debt reduction which is how I plan to accomplish the second pair of goals.

The next goal is more for the mental victory than anything else. I’m not maxing my 401k contribution yet, so this is technically not a priority. I think it would feel good to make the contribution even if it’s just $50.

Finally, I want to establish another income stream. Right now, most of my income is generated by my full-time job. I know that my investment portfolio is earning dividends, but I haven’t started tracking those. I’m not sure what form this new income stream will take at this time, but I do have a couple of ideas to explore.

Decelerate the Expenses

I’ve looked at a couple of areas on our variable monthly expenses and it looks like there are some easy wins to be had.

Expense Goals

- Meet the $800 per month grocery budget

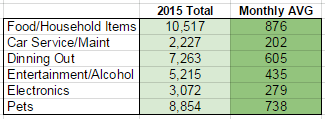

- Reduce dining out to $400 per month (2015 – $600)

- Reduce entertainment/alcohol to $250 per month (2015 – $435)

If we can accomplish these, we should be able to free up around $5500 in cash flow. We just need to make sure to stick to the meal planning schedule and have groceries ready for the week. I’ll be setting up a spreadsheet to track progress on that and help with accountability.

Let’s Talk Business

I’ve been reading a bit about business entities and the various benefits afforded to them. This year I plan to create my first business entity and being to explore what I can do with that.

While I don’t have any firm plans for what I want the business to accomplish quite yet, this exercise is more about learning the process at this point.

What about Chuck

When I started the blog, I talked about the canoe dock and what it means to me. That place is capable of centering me and I love the way I feel when I’m there.

This year I’m adding some personal goals as well in order to find that state of being more often. In 2015, I only took a total of six days away from work. That was back in March. With the crunch of project deadlines, the last half of the year was a bit stressful.

For 2016, I intend to take a little more time for myself.

Personal Goals:

- Meditate at least three days a week

- Take walks at least three days a week

- Spend at least seven days camping

- Go kayaking at least one time

- Take one family vacation

The first two items might be challenging as I’m not very good at establishing new routines. I’ll need to set up another spreadsheet to track progress and keep me accountable. There may also be apps that I can use on my phone to help.

The last three items should be pretty easy to do. My wife and I already have plans to hike part of the AT while our daughter is at summer camp. We also have a family vacation already scheduled.

That’s at least two weeks away from work which is much better than last year.

State of the Blog

My goals for the blog really haven’t changed much. I still want to continue to document my progress and record stories about relevant events in my life.

I have gotten a couple of comments from real people (Thank You!), so I know that I’m starting to reach an audience. If I could grow to ten comments in the new year, I think that would be just fine.

Happy Holidays

Thanks for stopping to see what’s happening here and I wish you the best in 2016.

Cheers!

-cb3